Inflation Is Stealing Your Time

An invisible thief, inflation unchecked can ruin you.

“Inflation is when you pay fifteen dollars for the ten-dollar haircut you used to get for five dollars when you had hair.” - Sam Ewing

When asked to define money, many Christians half-jokingly reply, “It’s the root of all evil.” Since the Apostle Paul did say “the love of money is the root of all kinds of evil,” I’d give that answer partial credit. That said, as we dive into a discussion about inflation in order to protect our wealth from it, let’s remember not to fall in love with money, okay?

My parents taught me to view money as a tool, not as a goal itself. This advice made such a deep impact on my thinking that it became part of my personal mission statement. But over the last two years, I’ve begun to view money through a different lens. I now view it as a store of time and energy. Sound pretty weird? Let me explain.

Let’s say you put in long hours and lot of energy working for your employer (or even better, for yourself). In return you receive a paycheck. With that paycheck, let’s say you purchase a Starbucks latte, which the barista spends time and energy to make. For your time and energy you receive money, and with that money, you in turn compensate another person for their time and energy. Thus money acts as a store of time and energy.

Perhaps now it’s easier to understand why I like to define wealth as the control of time. And while not the end-all-be-all of this life, wealth is important because time is precious. By wisely handling the money God has given us (by preserving and growing it) we can spend more time with our family, explore more of God’s creation, and better utilize our time and talents. I think that’s a worthwhile goal.

At this point, you should be able to follow my logic when I say I consider a theft of my wealth as a theft of my time. And you can be sure I wouldn’t take the theft lightly. Thankfully most of us haven’t been stolen from directly, but unfortunately all of us have had a run in, with an invisible thief. That thief is inflation.

Those encounters may have been while you were in the market to buy a car, or lumber, or a house, or simply your weekly groceries. In fact, recently it could have been while purchasing almost any good or service. All of a sudden, things just seem so dang expensive! These anecdotal observations, over the last year, were probably reinforced by headlines similar to the one below:

But is inflation really all that harmful? While many Americans are led to believe that inflation is simply a byproduct of a booming economy or a necessity of our modern economy, inflation is much more complicated than that. And it has serious consequences for those who remain unaware of its affects.

Let’s begin understanding inflation by defining it. Although many economist have differing definitions, two of the most common are, 1) when the amount of currency units increases (e.g. the number of US dollars increases), and 2) when the price of goods or services increases. I believe a complete discussion of inflation encompasses both of these definitions.

Inflation - defined as an increase of the supply of money - is addressed by the legendary economist, Milton Friedman. He said that inflation is:

“…always and everywhere a monetary phenomenon in the sense that it is and can be produced only by a more rapid increase in the quantity of money than in [economic] output.” (Yeah, that’s a mouthful!)

In summary, Friedman’s argues that inflation is created when a country issues currency (dollars) faster than it increases its production of goods and services. As an example, this is what occurred in the aftermath of the US government’s response to Covid-19. Trillions of dollars were “printed” and distributed, but Americans were working and producing less. Therefore, Americans were able and willing to pay more for the available goods and services. This caused the prices to rise - creating inflation.

As you can see, in explaining the first definition of inflation - an increase in the amount of currency - we also discussed the second definition - the rising prices of goods and services. Although an increase in the supply of currency is not the only cause of price hikes, it’s rare for one to occur without the other.

We’ve established what inflation is, but beside it hurting our wallets, what’s the big deal? The answer to that is, inflation becomes a big issue for individuals when it rises more quickly than their income and investments rise. This is happening to most Americans today.

Let’s use my situation as an example. Last year, I received a 2.6% pay raise. Pretty cool, right? Not cool when you realize that the Consumer Price Index (CPI) - the US government’s official inflation measurement - increased by 7% last year. So what that means is, I received 2.6% more pay, but my expenses went up an average of 7%. By that math, I became 4.4% more poor (7-2.6)! To just stay neutral, I would have needed a raise of 7%. Unfortunately, I’m not the only one in this boat. Did any of you received more than a 7% pay raise in 2021?

And it’s not just income. How about investments? If you’re the average American with a retirement account invested in a “60/40 plan” (aka 60% in stocks and 40% in bonds), that forty percent invested in bonds likely only gave you about 2.5% interest. In other words, it lost almost 5% of its value.

Unfortunately, that’s not the worst of it. It’s widely understood that the CPI severely underestimates the rate of inflation. Consider that if you were in the market for a home this last year, you would have seen an 18.6% increase in home prices. Additionally, the stats below show it’s not just homes that were way above the CPI:

Can the CPI, the US government’s official inflation number, be inaccurate? Yes it can, and likely is. The reason I can say that with confidence is because the government is in fact incentivized to keep the CPI artificially low. Consider a few examples: First, Social Security entitlement payments are increased each year at the rate of the CPI. So, the lower the CPI is, the less the government has to pay. Second, all government civilian and military paychecks and retirement payments are also increased in correlation to the CPI. Again, the lower the CPI, the less the government must pay these folks. These are just two reasons, among many, for the government to keep the CPI artificially low. And they’ve done it, rather successfully I might add, by changing how the CPI is calculated over the years.

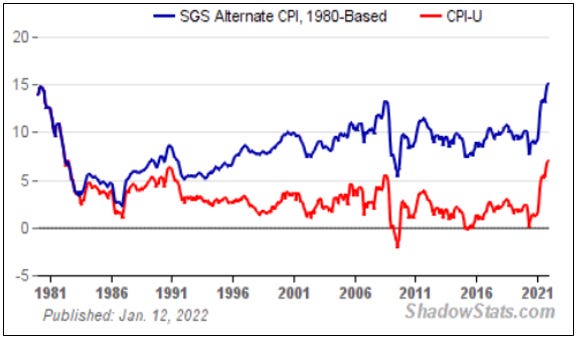

The Bureau of Labor Statistics controls and tracks the changes to the CPI. The affect of these changes is dramatic. Take a look at the chart below. The red line graphs the CPI number the government has reported. The blue line shows what the CPI would be if it hadn’t been changed dozens of times over the last forty years.

Because the government is incentivized to keep the CPI low, the probability is high that the changes are made to intentionally keep it low. Not a certainty, but a high probability.

The blue line in the graph above shows inflation in 2021 reaching 15%; not 7%. If you think about it, with an 18.2% price increase on homes, 24.4% on vehicles, and 22.1% on beef, 15% could easily be more accurate than 7%.

Let’s use myself as an example again to highlight the impact of this difference. If inflation is closer to 15%, that means I became…12.4% more poor in 2021. That’s crazy! How about for you?

You might be wondering how to respond to this information. Well, the unfortunate answer is, it depends. It depends on who you are, your goals, and your stage of life.

The goal of this discussion is to simply highlight the some possible consequences of high inflation. Without an understanding of these effects, it will be much harder for us to store up wealth, exit the rat race, and pass along a physical inheritance to our children, and grandchildren. So pay attention, increase your understanding, and take appropriate action.

There is so many more facets to and causes of inflation. One recommendation for learning more about how supply, demand, and inflation work is to check out Thomas Sowell’s fantastic book, Basic Economics. Use this newsletter as a starting point and motivation to begin developing your financial fitness.

And remember, the only financial advice the The Intrepid Life gives is…don’t fall in love with money!

Now get out there and live an unsafe, but good life.

P.S.